This article has been written by an expert contributor Marcus Today

Overview

Computershare (CPU) is a business that offers corporate trust, stock transfer and employee share plan services in a number of different countries. Most of its earnings come from operations outside Australia with the US its biggest contributor. Aside from fees for its services, CPU generates a large portion of its earnings from interest on client-owned cash balances (margin income) – which is a fairly defensive revenue stream.

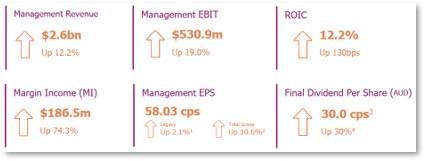

The stock recently finished down almost 5% on its results despite management EPS and management profit both coming in ahead of consensus and guidance. There was a high bar to reach given the upgraded guidance in February, which was reaffirmed in May and the share price appreciation since then.

Disappointment flowed from what some labelled a low-quality earnings beat as the result relied on a lower tax rate and higher margin income. A final dividend of 30c was declared, reflecting a 30% increase on last year. Guidance, which outpaced consensus, was considered conservative. CPU expects management EPS to increase by ~55% in FY23. Added to this, while inflationary pressures are impacting its operations, margin income, estimated to be around $520m this year, is anticipated to drive strong earnings growth.

Broker stuff

Brokers remain bullish, with the average target implying an upside of more than 22%. Citi upgraded to BUY following results, citing benefit from further increases in margin income, which is influenced by higher interest rates. UBS said FY23 guidance was ahead of expectations. Calculated every 50bp rise in the US cash rate adds $100m to its FY23 forecast and 13% to EPS. Currently, interest rates in the US are 2.25-2.5%, with expectations for it to reach 4% in 2023. The implication is that there is more upside to come. Macquarie said margins, costs and leverage all impressed as the company enjoyed the harvest of rising interest rates.

Risks

- Corporate Actions volumes are anticipated to be lower

- Employee Share Plans transaction volumes to remain volatile

- Cost pressures across all our business lines

- Mortgage origination volumes subdued

- Timing and extent of rate rises may differ to assumptions

Tailwinds

- Significant growth in margin income, driven by global rising rates environment

- Full-year contribution of Computershare Corporate Trust (acquired from Wells Fargo), including delivery of year 2 expected synergies and improved Money Market Fund fees

- Growing contribution from Governance Services businesses

- 2H Recovery in Bankruptcy volumes

- Ongoing focus on cost-out

A Curious Correlation

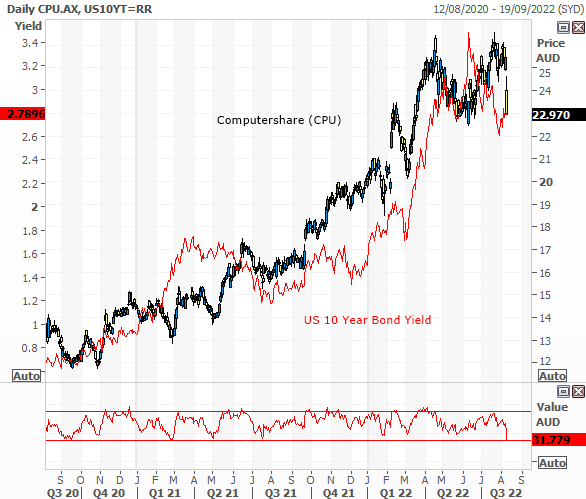

Computershare has been a beneficiary of higher interest rate expectations. That is clearly shown in the chart below, given its correlation coefficient with the US 10-year bond yield is greater than 91% or 0.91. Correlation coefficients are used to measure the strength of the linear relationship between two variables, in this case, the US 10-year bond yield and Computershare share price. A correlation of 1.0 indicates a perfect positive correlation, which means, the variables follow each other perfectly. Now at 0.913, there is a very strong suggestion that what happens to the US 10-year bond yield will also happen to the Computershare share price. While US bond yields have topped out in the short term, there is still a long road of rate hikes to come before the Fed calls the top, which means, there is still upside risk to the share price.

What sort of investment is CPU?

CPU is a mature business in good financial health. It operates a capital-light business model with a high proportion of defensive and recurring earnings. Its customer base is relatively sticky as switching between platforms can be costly and time consuming; the share registry client retention rate sits around 99% and the average client tenure is around 20 years. Safe data management and a commitment to capital management also help it maintain a competitive advantage. Majority of its earnings come from overseas and it reports in US dollars, so it enjoys an earnings tailwind from a weak Australian dollar.

Conclusion

Management is confident in the outlook and Brokers are all bullish. The share price has topped out, but it is still holding onto its long-term uptrend. Guidance for FY23 was solid and considered conservative. Given the sensitivity to higher interest rates in the US and the 150bp worth of rate hikes expected to come, CPU is shaping up into an attractive opportunity. BUY.

First published on 29th August 2022 on the Marcus Today website.

You can sign up for a free trial here.

Prior to making an investment decision, retail investors should seek advice from their financial adviser. This document is intended as general information only.