One company that enjoyed a lot of buzz in the covid years was Nintendo. Many investors looked at what Disney had done with their catalogue of intellectual property (IP) – turned it into movies, TV shows, theme park rides, live shows, cruises and so much merchandise – and wondered what other companies had similar catalogues of IP. With Pokemon, Mario, Link and Donkey Kong leading a deep catalogue of IP, Nintendo became a favourite of investors.

At the same time investors saw a lot of additional growth drivers in Nintendo’s hardware business. The IP of Disney and the gaming hardware of Sony – what was not to like?

The best example of a thesis on Nintendo from the covid years is this 122-page monster from Crossroads Capital.

A couple of years later, this article takes a look back at the thesis and how it has played out.

A lot has gone right for Nintendo. On an IP-side, headlined by the billion dollar success of the Mario movie. At the same time, the latest Zelda game sold just shy of 20 million units in a 3 month period.

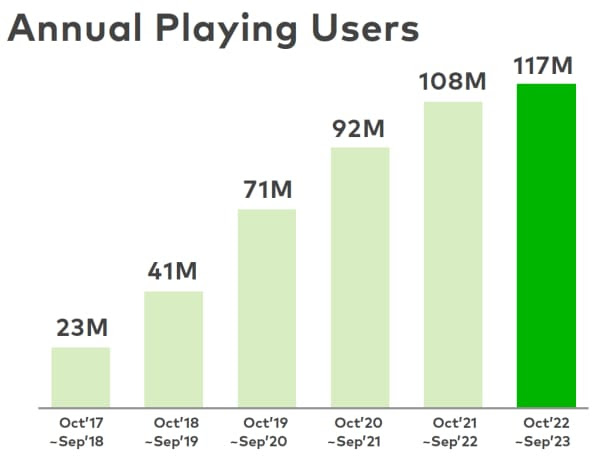

On the hardware side, the Nintendo Switch continues to sell, now surpassing 132 million units sold. This has helped push up Nintendo Switch’s Annual Playing Users to well beyond 100 million people.

But that isn’t to say there hasn’t been challenges. Nintendo has a mixed history with consoles, for example the Wii U selling only 13% of the Wii and leaving a particular black mark on the company’s memory. The Wii U failure saw Nintendo’s share price fall 85% and has made investors wary ever since. As Nintendo prepares for their next hardware investment cycle and to announce their successor to the Nintendo Switch (rumoured to be in the second half of 2024), investors around the world will be watching.

This is an excerpt from our Thought Starters email. Once a week we send you 5 interesting articles that have caught our attention, to get you thinking. No spam, we guarantee.