This article was written by expert contributor Matthew Haupt from Wilson Asset Management

The good news for equities is that financial conditions are likely to get easier in 2023, the bad news is we need a sharp deterioration in economic conditions and earnings to eventually induce these easier conditions. Bond markets are pricing a mild-to-deep recession, while stock markets are pricing a soft landing. Below we lay out five dominant themes that will drive markets in 2023.

- Falling inflation pausing the interest rate hiking cycle

- Job cuts before rate cuts

- Leading indicators reaching a trough will assist in a bottoming event for equities

- Australia will benefit from a resurgent China

- The global quest for mineral and energy security

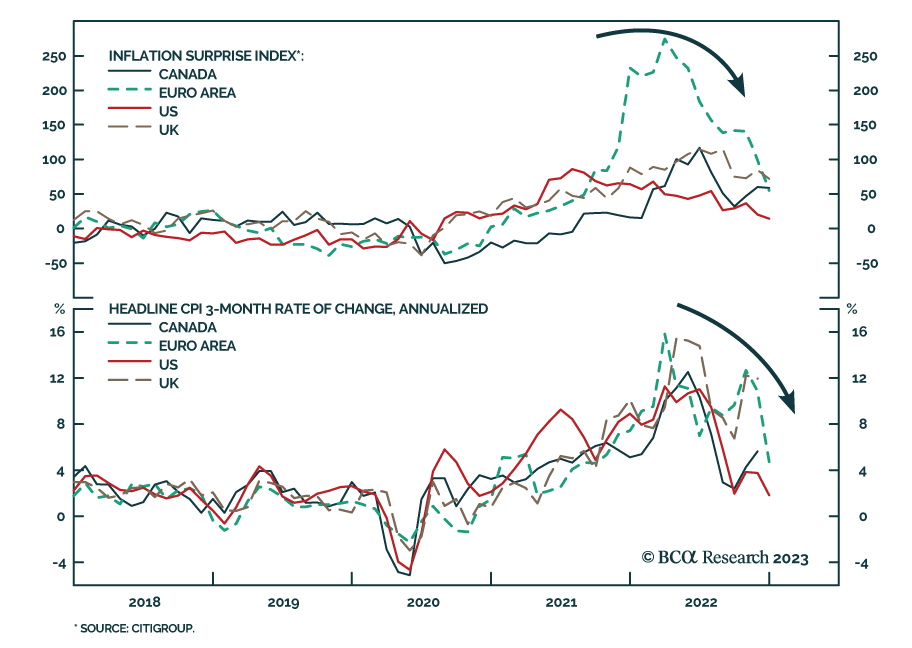

Falling inflation pausing the interest rate hiking cycle

Monetary policy action is determined based on lagging indicators, leading to a lag in the effects of their policy, often resulting in policy errors. In 2022, inflation soared above 9% in the US, 11% in the UK and 7% in Australia, and now almost 400 interest rate hikes across the globe later, it appears we have passed the peak. While inflation is still at an uncomfortable level above central banks’ lagging indicators and inflation targets, they are acknowledging that recent data indicates inflation is falling rapidly.

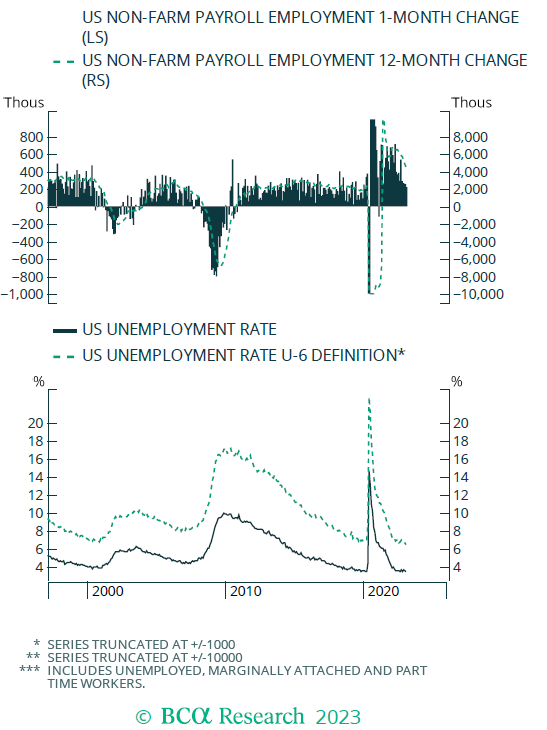

But rates won’t cut until there are job cuts

While falling inflation is celebrated as it implies we are nearing the end of the interest rate hike cycle, the job market is still running hot in central banks’ view (we hold an opposing view) and until this slows, central banks will likely keep financial conditions tight. Current market pricing implies rate cuts from November 2023. Rate cuts this year is a consensus view; the debate is around the speed and magnitude of cuts.

For rates to be cut faster than these lofty expectations requires a sudden softening in the labour market. Headline numbers are still strong, but based on previous cycles, the Fed will react incredibly quickly should this change. In previous cycles, central banks have only tolerated one or two months of job losses before adjusting policy. Over the next six months, job related data will be our most closely watched indicator given it holds the keys to future rate decisions.

Leading indicators reaching a trough will assist in a bottoming event for equities

As the excitement following a pause in interest rate hikes recedes, the concurrent economic data will worsen and the market narrative will likely turn to how deep the impending downturn will be. Leading economic indicators are currently painting a gloomy picture, which will spill over to the coincident numbers in the next few months and send earnings expectations lower; but being forward looking, the market will rally when leading indicators appear to have bounced off lows. With earnings rebasing and peak interest rates nigh, we expect mid-2023 will be a bottoming event for equities.

While we expect equity markets to find a floor, it won’t be a straightforward path. The range of potential outcomes continues to be wide, and expectations will remain volatile as we seek clarity around the depth and duration of the impending slowdown that is underway. Central banks are in a similar position of making decisions with imperfect information, and we could potentially be entering a ‘Greenspan’ era with frequent policy rate adjustments in both directions.

Australia to benefit from a resurgent China

A theme for 2023 will be the transition from a synchronised to unsynchronised world. China and Japan were the two outliers in 2022 when the world reopened and policy tightened. Japan is currently wrestling with yield curve control and keeping rates down, which has implications for the yen and broader foreign exchange (FX) markets, being the third most traded currency globally. China meanwhile has recently abandoned their lockdown strategy, while instructing local governments to speed up spending and relaxing property and developer rules. With all indicators pointing to a recovery, China will experience a very different 2023 to the rest of the world, even in light of softening exports. As Australia’s largest trading partner, a resurgent China should shield Australia from the full force of an otherwise global economic slowdown and support the AUD.

And the global quest for mineral and energy security

Globalisation had been a dominant, deflationary theme for the past two decades. This came to an abrupt end when the Trump Administration triggered a trade war with China, with ramifications for global supply chains as companies navigated the high tariffs. Next came COVID lockdowns exposing countries that were overly reliant upon imports to supply essential goods. In 2022, the Russian invasion of Ukraine further amplified the issues of energy and food security as large exports from Ukraine briefly halted while Russia continues to play games with Europe’s energy supply.

All these events have culminated into an urgent desire for countries to minimise their vulnerability caused by limited supply of energy, food and minerals, to the extent it is now a security issue being legislated. Australia is richly endowed with natural resources, which now demand a security of supply premium. Additionally, increasing demand for rare earths and battery minerals outside of China puts Australia in focus yet again.

So, how do we invest in this environment?

In summary, 2023 will be an incredibly challenging year for companies as they navigate a slowing economy. As talk around inflation fades, policy shift to fighting the economic slowdown will be underway. This is the environment to invest in high quality, yield sensitive, defensive names that will benefit from an eventual easing of financial conditions and are sheltered from the full severity of an economic downturn.

The good news for equity investors is we expect there will be a bottoming event through the year, which will produce opportunities to invest in sectors that benefit early in the cycle. However, this subdued economic environment is likely to be a multi-year story, where policy may oscillate as we experience sporadic slowdowns and accelerations.

At present, caution is warranted but we are working our way through a necessary process and hope to introduce more cyclical exposure to our WAM Leaders (ASX: WLE) investment portfolio later in the year.

WAM Leaders provides investors with exposure to an active investment process focused on identifying large-cap companies with compelling fundamentals, a robust macroeconomic thematic and a catalyst. The Company’s investment objectives are to deliver a stream of fully franked dividends, provide capital growth over the medium-to-long term and preserve capital.

Prior to making an investment decision, retail investors should seek advice from their financial adviser. This document is intended as general information only.