This article has been written by an expert contributor on 25th October 2022, Nimish Vyas, Global Market Strategist, J.P. Morgan Asset Management.

“Despite the rally over the past few days, the overarching concerns over inflation and monetary policy tightening will continue to be an uncertainty for risk assets over the short term.”

Nimish Vyas

Global Market Strategist

In brief

- With 23% of S&P500 companies (in terms of market capitalization) having reported, 3Q22 earnings have offered some positive surprises particularly in growth sectors of the equity market

- Initial earnings estimates expect a pickup in consumption and production activity over the quarter to be tailwinds, while headwinds consist of the subdued macro backdrop, increase in labor and freight costs, as well as an excess build-up of inventories

- Equity markets are responding positively, but overarching concerns over inflation and monetary policy tightening will likely take hold

Earnings have been better than expected so far

The S&P 500 gained 4.7% last week and continues to rally during the early parts of this week, as stronger than expected earnings buoyed investment sentiment, giving investors some respite from inflation concerns and the recent rise in Treasury yields. At the time of writing, more than 23% of S&P 500 companies in terms of market capitalization have reported earnings, with 53% beating initial operating earnings per share expectations. In particular, the better-than-expected earnings were driven by growthier parts of the equity market such as information technology and health care.

What to expect for the remainder of 3Q22 earnings

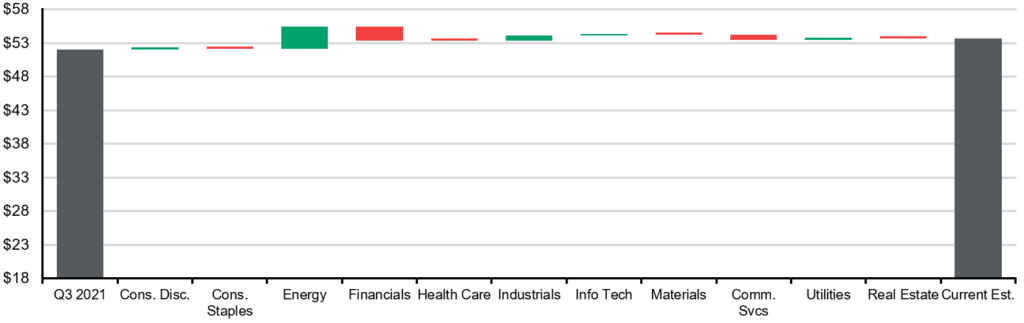

Our current estimate for 3Q22 S&P 500 operating earnings per share (EPS) is $53.68, representing a year-over-year (y/y) growth of 3.2% and a quarter-over-quarter (q/q) growth of 14.5%.

The strong estimates are supported by a number of tailwinds, including higher energy prices, a resumption in travel during the summer, and positive industrial production and retail sales data. That being said, there is also a considerable set of macro headwinds, which could push actual earnings to come in below projections. The U.S. dollar strengthened 16.7% y/y during the quarter, which, coupled with deteriorating conditions in Europe and continued COVID-19 lockdowns in China could weigh on foreign –sourced sales. Furthermore, early reporters have noted additional headwinds of softening consumer demand and higher prices, increasing labor costs, higher freight costs, and a build-up of excess inventories.

S&P 500 EPS contribution by sector

3Q22, operating earnings

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. All data are as of 24/10/22.

At the sector level, energy is projected to lead the pack due to higher crude oil and natural gas prices in Q3. Similarly, estimates indicate a strong quarter for industrials. Within industrials, the airline companies are expected to see profit growth decelerate due to increasing costs relative to demand but are expected to stay profitable. Transport should also be abright spot, as the rail companies benefit from higher volumes and higher pricing due to fuel surcharges. Materials are likely to be weaker due to a pullback in commodities prices and the sector’s higher exposure to foreign markets. Financials are expected to contract, primarily due to a build-up in loan loss provisions, weak investment banking activity, and slower loan growth. However, higher interest rates and market volatility may help partially offset these pressures by boosting net interest income and trading revenues.

Turning to growth, consumer discretionary could be well supported, in contrast to recent quarters, by demand for services, although preliminary reports have highlighted softening consumer demand in retail and production issues at auto companies. Despite the stronger-than-expected set of earnings from health care and information technology sector so far, we expect to see more subdued rates of growth in earnings as further earnings reports come through. Among the health care names, COVID-19 vaccine and testing sales are expected to be down from their peak in 3Q21 and will act as a drag on profit growth. In information technology, persistent inflation and fears of a global slowdown have seemingly hurt demand for hardware, with a number of firms announcing plans to scrap production increases and cut spending. Communication services is tracking a much sharper decline than its growth peers, as analysts are pessimistic about the sector’s ability to grow streaming and gaming subscriptions in the current market environment.

Similar to the prior quarter, operating leverage, which is defined as the change in operating income from a 1% change in revenues, will be key for profitability. Value sectors tend to have more operating leverage than growth sectors. Profits in sectors with greater operating leverage should be more resilient given elevated inflation over the next few months, but as economic growth begins to slow and inflation cools, we may see investors rotate back into growthier parts of the market.

Investment Implications

Despite the rally over the past few days, the overarching concerns over inflation and monetary policy tightening will continue to be an uncertainty for risk assets over the short term. While 3Q22 earnings have offered a positive surprise and equity valuations are looking cheap, we maintain a preference for fixed income over equities. For those equity investors with less sensitivity to volatility, better than expected earnings results in the third quarter will offer some comfort about the potential impact of sub-trend economic growth, however we continue to advocate for a focus on quality and defensive sectors as well as short-duration equities with less sensitivity to rising discount rates.

Nimish Vyas is a research analyst on the J.P. Morgan Asset Management Global Market Insights Strategy Team. In his role, Nimish is responsible for supporting the team’s strategists in delivering timely market and economic insights to clients across the country. Nimish focuses specifically on U.S. equities, alternatives and the fixed income markets. Nimish joined the team in December 2020, prior to which he worked as an analyst at BNP Paribas. Nimish obtained a B.A. in Economics along with minors in Applied Mathematics and Financial Economics from the Johns Hopkins University in 2019.