This report has been prepared by Claremont Global

Growth in ESG awareness

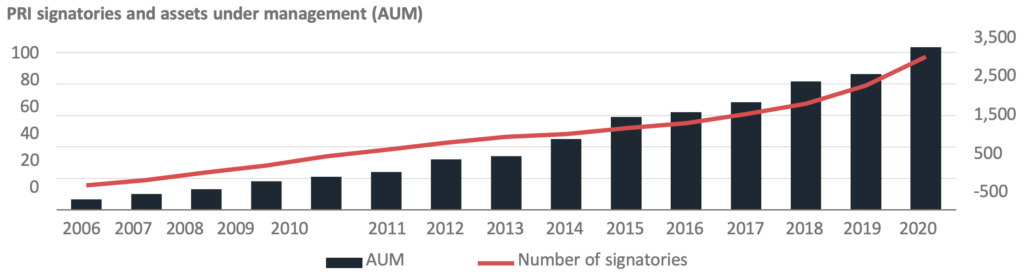

ESG awareness among investors continues to increase on a global scale. This has been made most evident via the growing prominence of the United Nations Principles for Responsible Investment (PRI) among institutional investors.

Launched in 2006, the PRI was initially established to raise awareness of Environmental, Social and Governance (ESG) considerations among the investment community, as part of developing a more sustainable financial system.

Since that time the PRI has become the world’s leading proponent of responsible investment and as of 2020 exceeded 3,000 signatories and represented over US$100 trillion of assets under management.

Alignment with our investment framework

With a central focus on sustainable long-term company performance, the Claremont Global Fund is now a signatory to the PRI. Whilst a new and welcome development, in reality we expect there will be little change to our proven investment process.

Our underlying strategy and our rigorous research-backed process naturally leads to investment in well-run businesses with strong management teams and a culture attuned to the long term needs of all stakeholders.

Since the inception of the strategy in 2011, our goal has been to generate returns of 8-12 per cent per annum, through the cycle, for our investors. We have always stressed to clients the importance of keeping a long-term perspective.

Our ability to achieve this requires us to remain true to our investment process and invest in sustainable businesses – something we believe is largely unachievable, without serious consideration of ESG principles. Research has shown that when companies adopt good ESG policy it’s a positive for all stakeholders, which includes improving financial performance for investors.2

Relationship to our investment pillars

Our philosophy and process are based on four key investment pillars:

Management quality and ESG

We believe that a first-class ESG approach is unlikely to have a tick-the-box methodology. Rather, it is driven by the principles, values and, most importantly, actions that underpin company culture. This flows from the actions of management and the board of directors – with management quality one of the fund’s key investment pillars, (or in ESG parlance, a focus on good governance).

This requires a long-term mindset; a focus on delivering value to customers; equitable treatment of employees and communities; and continuous operational improvement that benefits all stakeholders.

Our experience is that this long-term mindset is typically found within stable, well-tenured management teams – it is unlikely to be built overnight – and is something we seek in all the companies we invest.

However, culture is more difficult to measure and requires some judgment on our behalf.

With a relatively finite universe of companies that meet our quality investment criteria, we can consistently engage with management teams, allowing us to better assess management’s mentality and actions, and gain deeper insight into the prevailing culture. Prior to investment in a company, we will always speak with ex-employees, competitors and industry experts where possible.

We also look at the composition of the executive team and board, tenure and strategy. This, we believe, allows us to pass both an independent and educated judgement on a key facet of a business that cannot be screened for, lifted from a broker report, or extracted from an ESG score from one of the rating agencies.

Capital structure and ESG

A strong balance sheet – another of our key investment criteria – is often illustrative of good governance, and is an area frequently overlooked, due to a focus on maximising short-term profitability.

Companies that engage in ‘financial engineering’, such as taking on excessive debt to reward shareholders in the short-term, through share buybacks and poor M&A – only to then go seeking government and/or shareholder assistance in times of crisis – is in our eyes a complete governance failure.

Our process deliberately aims to keep us clear of such businesses and industries, allowing us to research and ultimately invest in businesses that are managed to successfully navigate, and indeed prosper, through adverse economic events.

The average age of the companies in our portfolio is currently over 80 years and these businesses have seen many economic cycles and stood the test of time. Their durability is a combination of tested business models; the value proposition they offer their customers and employees; and prudently managed balance sheets.

It is difficult to overstate the power of incentives and we always analyse management compensation closely.

We engage with our companies regularly (at least quarterly), highlighting what we believe are important considerations, as well as voting on the remuneration of executives on an annual basis.

Incentives for some companies are skewed to short-term financial metrics (such as “adjusted EPS”) and a misaligned remuneration structure may lead to short-term gains, but result in perverse outcomes both for the broader community and ultimately for the longer-term shareholder.

When considering the Environmental impact of a business, we find that management teams with a strong culture and good ethics, coupled with the right incentives, are comfortable investing in areas such as energy and water efficiency, waste reduction, and/or proper remediation of historical environmental issues.

These investments can often have a negative impact on short-term profitability but deliver long-term benefits, ranging from reduced carbon emissions, employee safety, favourable reception by local communities, regulators, and customers – all while reducing operating costs over time.

As a result, we prefer to see a large proportion of management compensation based on a variety of long-term metrics such as organic growth, margins, cash flow and return on invested capital, rather than measures such as ”adjusted” EPS, which can be more easily manipulated in the short term.

Business quality and ESG

Of course, a definition of business quality is broader than simple financial metrics.

In the past, Social issues may have been limited to the human resources division, however, today they expand far beyond this narrow remit.

For us, social considerations cover the relationships the company has within its ecosystem. From the impact the company’s products/services have on communities, to the treatment of their employees, places of manufacturing and suppliers. We have no doubt that failure to adequately respect all subsegments of a company’s value chain will impair the long-term sustainability of a business.

Globalisation, transparency, investor awareness and ESG are increasingly (and rightfully) calling into question how a company’s profits are made. We routinely engage with management to better understand whether they may be

compromising on the quality of their product/service (for example, buying materials from a cheaper source that does not adhere to local emission or labour practises) to simply meet a short-term financial objective.

We believe such actions are not sustainable over the long-term but also highlight management’s failure to seriously consider the impact of their business on society and the culture of the organisation.

Identifying quality growth businesses for the long-term

Despite the best intentions, the rise of ESG within the investment community has not been spared the hype that generally accompanies an emerging area of interest where financial gain is possible.

Increasingly, the industry is looking to capitalise on the trend, launching “green” funds (which often come with higher fees), while investors have looked to profit from the share price appreciation of companies they think will be beneficiaries of ESG- focused buying.

With a clear focus on capital preservation, investors in our fund can take comfort that we will remain disciplined when it comes to the price we pay for businesses and exercise caution by avoiding areas of speculation and thematic investing.

As illustrated, the principles of ESG have been – and will continue to be – critical to our investment process and our portfolio of companies.

However, ESG factors are nuanced and typically cannot be reduced to specific metrics or rules that are comparable across businesses. As a result, we believe it is prudent to use independent judgement and consider each business on a case-by-case basis, rather than be governed wholly by externally generated ESG metrics.

To conclude, whilst ESG in the mainstream is a relatively new phenomenon, our investment process has always emphasised management teams with a strong commitment to their customers, employees, communities and wider society. We believe when these factors are combined with good governance and prudent balance sheets, the end result is better risk-adjusted outcomes for long-term shareholders like ourselves.

This report has been prepared by Claremont Funds Management Pty Ltd (Investment Manager) (ACN 649 280 142, ABN 38 649 280 142, CAR No. 001289207), as investment manager for the Claremont Global Fund (ARSN 166 708 792) and Claremont Global Fund (Hedged) (ARSN 166 708 407), which are together referred to as the ‘Funds’. Equity Trustees Limited (ACN 004 031 298, AFSL 240957) (“Equity Trustees”) is the Responsible Entity of the Funds. For further information on the Funds please refer to each Fund’s PDS which is available at www.claremontglobal.com.au. This report may contain general advice. Any general advice provided has been prepared without taking into account your objectives, financial situation or needs. Before acting on the advice, you should consider the appropriateness of the advice with regard to your objectives, financial situation and needs. Past performance is not a reliable indicator of future performance. Future performance and return of capital is not guaranteed. The information may be confidential and is intended solely for the addressee. If you are not the intended recipient, any use, disclosure or copying of this information is unauthorised and prohibited. If you receive this e-mail in error please notify the sender and delete the e-mail (and attachments). This report may contain statements, opinions, projections, forecasts and other material (forward-looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. The Investment Manager and its advisers (including all of their respective directors, consultants and/or employees, related bodies corporate and the directors, shareholders, managers, employees or agents of them) (Parties) do not make any representation as to the accuracy or likelihood of fulfilment of the forward-looking statements or any of the assumptions upon which they are based. Claremont Funds Management Pty Ltd is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457), a signatory to the United Nations Principles for Responsible Investment (UNPRI). Actual results, performance or achievements may vary materially from any projections and forward-looking statements and the assumptions on which those statements are based. Readers are cautioned not to place undue reliance on forward-looking statements and the Parties assume no obligation to update that information. The Parties give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this report. The Parties do not accept, except to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this report. Any recipient of this report should independently satisfy themselves as to the accuracy of all information contained in this report. MSCI indices source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representation with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.